Education

In the UAE, End-of-Service Benefits (EoSB) have traditionally been treated as a statutory requirement, calculated and accrued on employers’ balance sheets throughout the period of employment, and paid out when an employee leaves the company. For many organisations, it has remained a standard part of doing business, addressed only when necessary but rarely discussed beyond payroll and compliance.

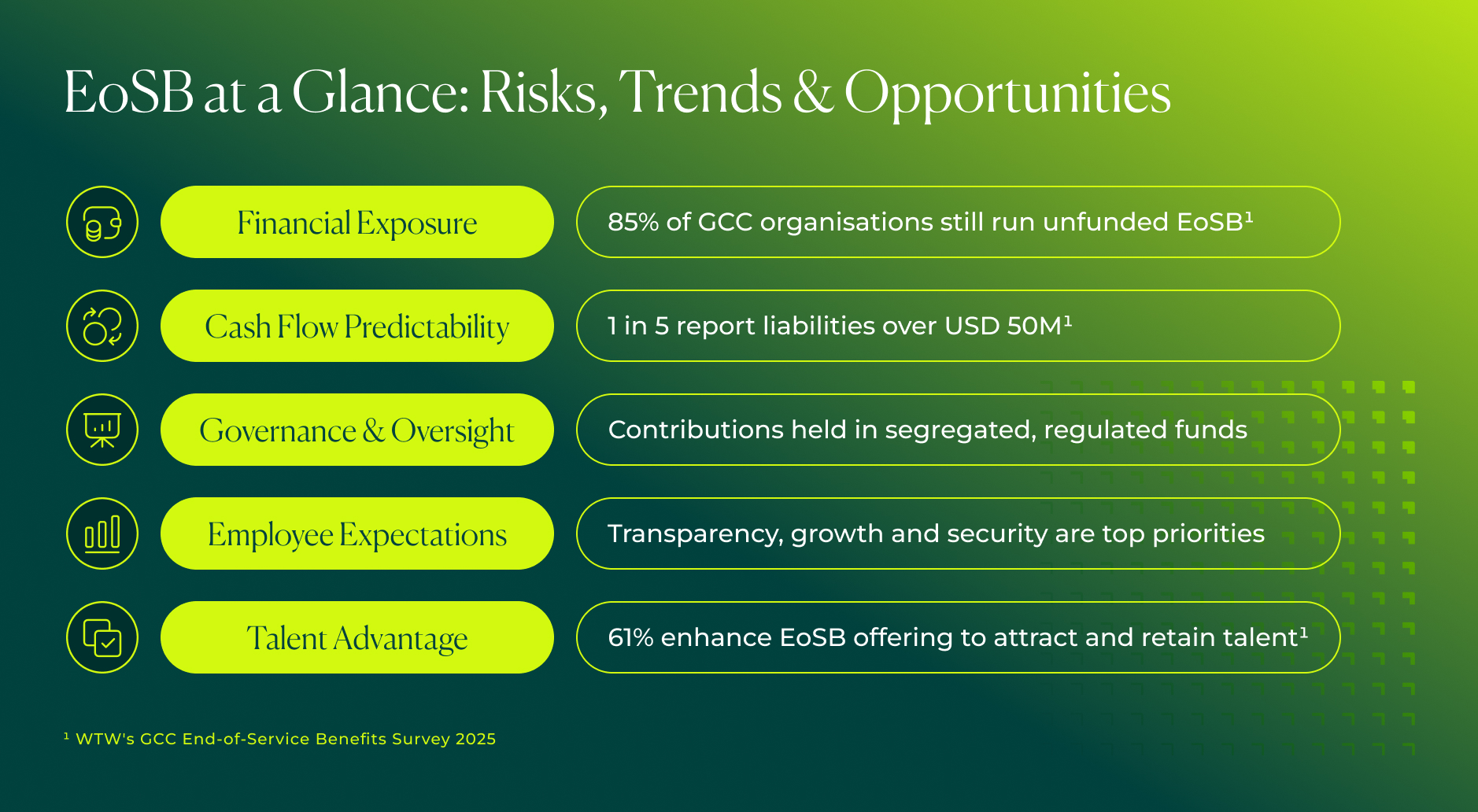

That is beginning to shift. Today, EoSB sits firmly on the agenda of finance and leadership teams, not just HR, because it influences cash flow planning, balance sheet exposure, governance standards, and how organisations position themselves in a competitive talent market.

The introduction of the Alternative End-of-Service Benefits Scheme in the UAE has expanded the options available to employers and introduced a more structured approach to managing these obligations. The conversation is no longer about meeting minimum requirements. It has evolved to whether the current structures support financial resilience and long-term business strategy.

Under the traditional structure, end-of-service benefits accumulate on the company’s books and are settled as a lump sum when employment ends. Until that point, the full obligation remains with the employer.

According to WTW's GCC End-of-Service Benefits Survey 2025, one in five organisations report end-of-service liabilities, the total amount owed to employees at the end of their service, exceeding USD 50 million. Most organisations continue to operate unfunded arrangements, which means they do not set aside money in advance to cover these future payments. For larger or long-established businesses, these figures are not unusual. They reflect how significantly gratuity obligations can grow over time.

The issue is not simply the size of the liability. It is whether leadership teams have clear visibility over its trajectory and a defined strategy for managing it. When obligations are carried internally without progressive funding, exposure compounds quietly in the background. The survey notes that 85% of organisations still have unfunded EoSB arrangements, which can lead to sudden pressure on cash flows and heightened risk during periods of economic volatility. Moving to a structured, funded model not only improves transparency but also allows companies to plan ahead and reduce unexpected financial shocks.

Workforces are rarely static. Growth, restructuring, market changes, and employee movement all affect turnover. Under a lump-sum gratuity model, large payments are required when employees leave. Periods of sudden, widespread workforce change, such as those seen during the COVID-19 pandemic or other unexpected events, can result in several employees exiting around the same time and create significant short-term pressure.

The Alternative End-of-Service Benefits Scheme changes this dynamic. Contributions are made monthly into regulated funds, linking funding to time in service rather than exit events. The obligation itself does not change, but its impact on the business does. Instead of facing sudden payout spikes during times of change, funding is spread steadily over time. In fast-moving markets, this matters. It allows businesses to plan workforce decisions around long-term strategy rather than immediate cash pressures.

Governance expectations across the region continue to rise. Boards, investors, and stakeholders increasingly expect clarity around how long-term liabilities are managed.

Within the alternative EoSB framework, contributions are placed into professionally managed funds and held separately from employer operating accounts. This structural separation reduces reliance on company liquidity at the time of payout and introduces regulatory oversight into the funding process. It also ensures that employees’ EoSB funds are secure and separate from any financial obligations of the company in case of business difficulties.

A funded and segregated structure signals financial discipline. It demonstrates that obligations are being proactively managed rather than deferred. For organisations focused on strong governance, the way end-of-service benefits are structured shows how seriously they manage long-term financial risks.

The UAE workforce is evolving, with more professionals choosing to build longer careers in the country. For many employees, financial wellbeing is no longer a back-end consideration; it directly influences career decisions and loyalty.

Traditional gratuity provides certainty, but it only comes at the end of employment and offers limited visibility along the way. Alternative EoSB structures give employees transparency, control, and the potential for their benefits to grow throughout their tenure.

The key question for employers is whether the current benefits approach reflects what employees value today: security, clarity, and the ability to plan confidently for the future.

End-of-service benefits increasingly form part of the broader employee value proposition, with 61% of organisations enhancing their EoSB frameworks, citing talent attraction and retention as the primary driver, according to WTW's GCC End-of-Service Benefits Survey 2025.

This reflects a shift in mindset. Employers are recognising that how benefits are structured communicates intent. It signals whether the organisation is forward-looking, transparent, and prepared to invest in their employees’ long-term financial wellbeing.

In competitive industries where professionals evaluate the full employment offering, the structure of end-of-service benefits can shape perception as much as overall salary. A thoughtfully designed and well-governed EoSB framework reinforces credibility and commitment to sustainable workforce planning.

Today, the Alternative End-of-Service Benefits Scheme has transformed the landscape for UAE employers. The choice is no longer simply about meeting statutory requirements, but about taking control of exposure, improving predictability, and demonstrating strong governance and employer brand.

Organisations that approach EoSB strategically can better manage risk, strengthen both financial resilience and employer reputation over time, and position themselves as employers of choice in a competitive market.

As a pioneer in the UAE, Ghaf Benefits sets the standard for modern end-of-service benefits. Operating as a MOHRE-approved and CMA-regulated solution, Ghaf Benefits enables employers to transition from internal accrual to structured, professionally managed funding. With a focus on regulatory oversight, governance, and simplicity, Ghaf Benefits is the partner of choice for organisations seeking to align their end-of-service structure with financial discipline and long-term vision.

Have you seen Ghaf Benefits featured in the latest Gulf News article? You can read the full article on the Gulf News website here.

1 GCC End-of-Service Benefits Survey 2025 (https://www.wtwco.com/en-ae/insights/2026/01/the-changing-landscape-of-end-of-service-benefits-in-the-gcc)

The Lunate End of Service Benefits Fund (“Lunate EoSB”), known as the Ghaf Benefits Plan, is managed by Lunate Capital LLC and its affiliates. The material provided is for informational and educational purposes only, not investment, legal, tax, accounting, or professional advice, nor an offer to buy or sell any securities or products. Recipients should seek independent professional advice before making decisions. Past performance or historical data are illustrative only and not indicative of future results, and forward-looking statements involve risks and uncertainties. Lunate does not guarantee the accuracy, completeness, or reliability of the material and disclaims liability for any losses, damages, or errors arising from its use. Redistribution is prohibited without prior written consent. While the Lunate EoSB is authorised by the UAE Capital Market Authority (CMA), such authorisation does not represent endorsement or guarantee.

If you need additional support or have any questions, our team of experts is here to help and guide you.

Get in touch